{kind=link}

WASHINGTON — Virginians in flood-prone areas have more than just rising sea levels to worry about. They have rising flood insurance rates to worry about too.

Many Virginians who get flood insurance through the National Flood Insurance Program will have to pay more under the Federal Emergency Management Agency’s new model for calculating rates, which went into effect last year for new policyholders and will be used for current policyholders when they renew their policies. The changes have sparked criticisms that FEMA is not being transparent about the new calculations, with Virginia’s attorney general joining a federal lawsuit challenging them.

“It’s a complicated beast,” said Mary-Carson Stiff, director of the environmental nonprofit Wetlands Watch, which has worked with several local governments in Virginia on NFIP requirements. “It’s the government providing insurance, so what could go wrong?”

Here’s what to know.

How it works

People largely voluntarily enroll in the NFIP, although those living in homes with government-backed mortgages in high-risk flood areas known as special flood hazard areas are required to have insurance through either private companies or the NFIP.

The program was created in 1968 by the National Flood Insurance Act. It currently serves 5 million policyholders nationwide, protecting $1.3 trillion in assets.

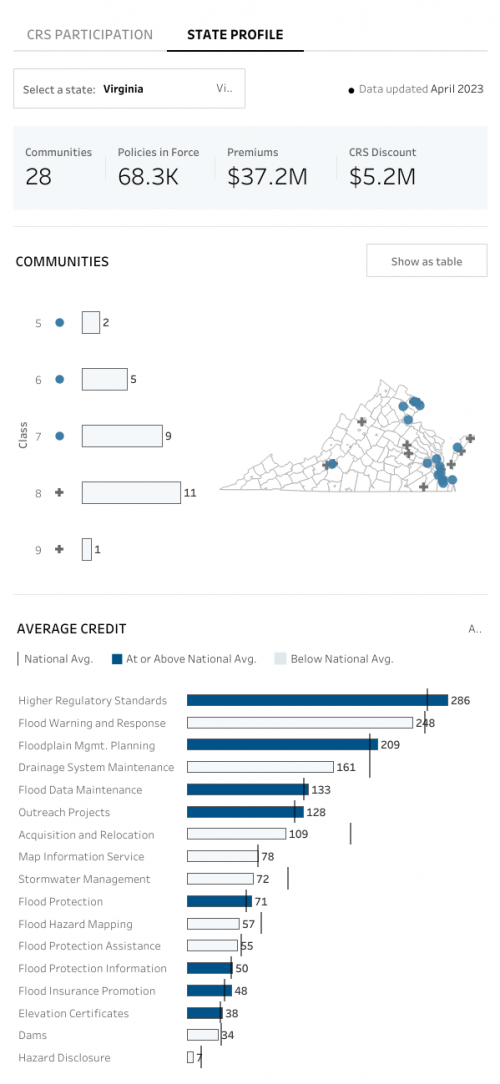

In Virginia, there are 94,920 policyholders in 291 counties, towns and cities.

Residents can get policies by reaching out to their home or auto insurance provider. In Virginia, there are 24 providers, including Allstate, Liberty Mutual and USAA. If people can’t get insurance through their regular provider, the NFIP will offer coverage.

The policies cover up to $250,000 for building damage and $100,000 for building contents. Commercial properties are protected up to $500,000 for building damage and $500,000 for contents.

According to FEMA, 1 inch of water can cause $25,000 worth of damage to a home.

Over the years, the NFIP has also had debt problems. According to a Congressional Research Service study, the program has had to borrow money following several major storms. The latest congressional spending authorization reduced its borrowing ability from $30.4 billion to $1 billion.

What the goals are

The NFIP was designed to protect people’s property lost to flooding and encourage communities to adopt adequate floodplain management regulations to mitigate flood damage.

Some 99% of the country’s counties were impacted by a flooding event between 1996 and 2019, with $53,000 being the average payout for losses and $700 being the average annual flood insurance premium.

In Virginia, since 1996, flooding events peaked at almost 600 in both 2003 and 2018. The only other year to surpass 400 flood events was 1998.

The flood events have mostly happened in Northern Virginia, the Piedmont region and the eastern part of the Shenandoah Valley, with over 50 in total since 1996. The rest of the state has had around 20 to 30 events.

While logic would presume that more coastal areas would have higher numbers of flood events, Stiff noted that most hurricanes don’t land on Virginia’s coast.

“Many of the hurricanes have landed in the Carolinas, then moved up the middle of the state,” Stiff said. “We see this occurring with many storm systems.”

To encourage local governments to adapt to and prepare for flooding, FEMA administers a Community Rating System that incentivizes localities to adopt floodplain management measures by allowing their residents to receive discounts on their premiums.

The more measures a locality adopts, such as having elevation requirements in the building code or conducting outreach to educate residents on flooding, the better the rating it receives and the higher the discount on premiums that is available.

There are 28 localities participating in the CRS in Virginia, with most on the coast and in Northern Virginia. Roanoke City and Roanoke County are the only localities in Southwest Virginia to participate.

“It’s a monumental effort,” said Rachel Pence, environmental specialist and CRS coordinator for the city of Roanoke, noting she frequently collaborates with mapping and building code officials.

While acknowledging that rural areas of Virginia are not immune to flooding — as in the major 1985 flood in the Roanoke River Valley — city of Roanoke Stormwater Manager Ian Shaw surmised that other localities may not participate in the CRS program because of a lack of staffing that the city is “fortunate to have.”

In addition to conducting targeted outreach for residents in flood-prone areas, Roanoke City also has attained grants to buy and demolish properties at risk of recurrent flooding, such as a Ramada Inn Conference Center on Franklin Road, in order to maintain the lot as open space and prevent future development on it.

Out in the more rural parts of the region, Roanoke County was among the first in Virginia to participate in the CRS program in Virginia in 1991. Butch Workman, who has coordinated the program for the county since then, said higher building elevation requirements have led to residents collectively saving $40,000 to $50,000 a year for flood insurance policies.

“They know me, I’ve sent letters out to them ever since 1991,” Workman said of his relationship with residents. “It’s made the county more aware.”

In Virginia’s coastal region, James City County is among the communities with the lowest — or best — CRS ratings, with policyholders receiving a 25% discount on premiums and seeing savings of over $100,000 in total annually. The locality has 860 buildings within the floodplain.

Toni Small, director of the county’s Stormwater and Resource Protection Division, in an email said James City is “very much aware of the efforts (studies and models) by the Hampton Roads Planning District Commission (HRPDC) to determine impacts that may occur as a result of rising sea level and/or increased precipitation, both of which may increase the potential for even more flooding impacts to James City County in the future.

“Rather than simply reflecting savings on insurance premiums, all of these steps are being done to reduce and avoid flood damage to insurable property,” she said.

How much rates are rising

In 2019, flood insurance policyholders in Virginia had an average yearly premium of about $737, or $61.40 a month. By comparison, in 2022, auto insurance in Virginia cost $1,066 on average annually.

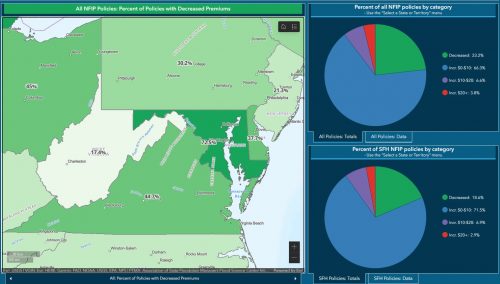

According to FEMA, the new model will result in 48.6% of Virginia policyholders seeing an increase in their monthly payment of up to $10, with 4.9% facing an increase of $10 to $20 and 1.8% an increase of over $20. Almost 45% will end up with cheaper premiums.

What the changes are

The old model largely based rates on the elevation of homes in flood-prone areas. The new model incorporates many more variables, but critics say FEMA has been tight-lipped on what exactly the changes are that are leading to increased rates for policyholders.

The new variables include flood frequency and the risk of different flood types from river overflow, storm surge, coastal erosion and heavy rainfall. Other variables include replacement cost values, which are typically lower for lower-income households, a factor that FEMA says will lead to lower rates and be more equitable.

“The current pricing methodology represents a significant step on the path to a solvent, financially sound and equitable program,” said FEMA Press Secretary Jeremy Edwards. “The NFIP’s new rating methodology levels the playing field for all policyholders.”

Overall, Edwards said, the new methodology “fundamentally improves the flood insurance landscape with its modern risk-based, property-specific, and actuarially sound rating system at a time when the nation faces more severe, intense, and frequent impacts from flooding.”

But for Stiff and one insurance provider in Hampton Roads, it’s unclear how the variables are actually calculated.

FEMA has posted calculations on its website, but “but there are still some missing elements,” Stiff said. “It is not the full picture of information required to fully understand a policyholder’s rate.”

Michael Vernon, founder and CEO of Flood Insurance Hampton Roads, said he’s seen a decline in flood mitigation projects policyholders are undertaking for their homes since the new model went into effect because fewer discounts are being awarded for them and it’s not clear how certain factors are weighted in calculations. Some policyholders who are farther away from water are seeing annual premiums of $2,800, whereas others closer to the water are seeing premiums of $900, he added.

“It’s all Greek to me,” said Vernon. “It makes no sense.”

A lawsuit by Virginia and nine other states

Louisiana and nine other states that are seeing rate increases have filed a lawsuit challenging FEMA’s new model. Virginia Attorney General Jason Miyares has signed onto the suit, with support from Secretary of Natural and Historic Resources Travis Voyles, who has argued the changes will lead to a potential loss in the state’s tax base.

“As rates increase, many homeowners, business owners, and renters in Virginia are likely to be priced out of their properties and forced to move out of Virginia, which will decrease Virginia’s tax base and therefore its financial ability to protect its residents and their property from flooding and flood damage,” Voyles wrote in a declaration filed with the lawsuit.

Voyles specifically points to changes in how elevation of homes will no longer lead to lower premiums, as it did under the previous model. He also noted Virginia has routed significant amounts of money through the Community Flood Preparedness Fund into programs designed to deal with flood issues.

FEMA and the attorney general’s office declined to comment on the pending litigation.

A hearing on the states’ request for the new model to be halted is scheduled for Aug. 11.

Virginia Mercury is part of States Newsroom, a network of news bureaus supported by grants and a coalition of donors as a 501c(3) public charity. Virginia Mercury maintains editorial independence. Contact Editor Sarah Vogelsong for questions: [email protected]. Follow Virginia Mercury on Facebook and Twitter.